AI's $600 Bn hole. Nobody is making money except😳

The Willy Wonkys

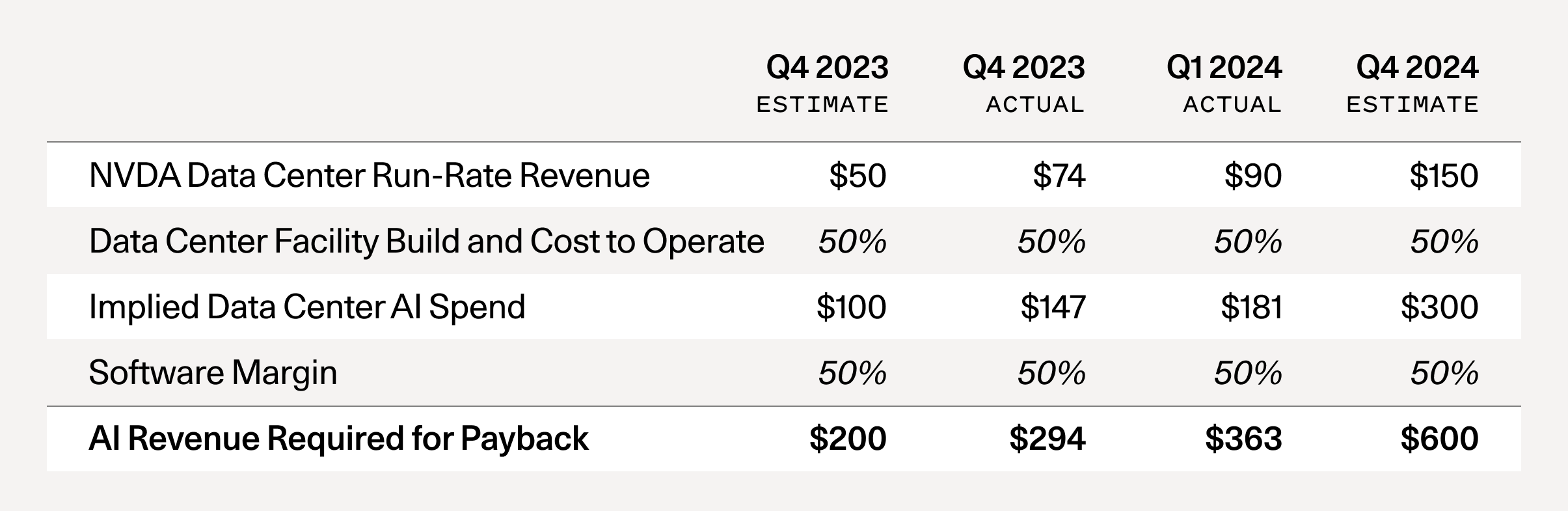

The AI bubble is for real and the best way to understand if this bubble is for real or not is to look at the capex investment vs. revenue growth in the AI ecosystem. Here is the data point (via David Cahn of Sequoia Capital).

Gen AI is resulting in $600Bn capex hole globally. A hole that needs to be filled for each year of CapEx at today’s levels.

All you have to do is to take Nvidia’s run-rate revenue forecast and multiply it by 2x to reflect the total cost of AI data centers (GPUs are half of the total cost of ownership—the other half includes energy, buildings, backup generators, etc).

Then you multiply by 2x again, to reflect a 50% gross margin for the end-user of the GPU, (e.g., the startup or business buying AI compute from Azure or AWS or GCP, who needs to make money as well) - source

OpenAI is the only winner ..so far

When it comes to consumer apps, OpenAI is the only winner so far. OpenAI’s revenue is rumored to be ~$3.4B, up from $1.6B in late 2023 - and while there are many startups doing <= $100mn ARR, nobody is even close to OpenAI.

The big question is outside of ChatGPT, how many apps have gone mainstream? Used by millions? (FYI: Perplexity did $20mn ARR last year).

That begs us an important qn:

So who is making money in Gen AI world?

The wonky ones.

You don’t want expect them to win..but they are.

Keep reading with a 7-day free trial

Subscribe to NBW: Startups, AI and Audiobooks to keep reading this post and get 7 days of free access to the full post archives.

| A guest post by

|